Federal Reserve Chair Jerome Powell has signaled a possible interest rate cut in September, saying that the “balance of risks” in the economy could be shifting away from inflation and toward rising layoffs.

Powell delivered the guidance in a highly anticipated speech on Friday at the central bank’s annual symposium in Jackson Hole, WY. It followed months of pressure from President Donald Trump and his allies on the Fed to cut interest rates.

“In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation,” Powell said in his remarks. “Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

Financial markets clearly interpreted Powell’s comments as signaling a rate cut at the Fed’s next policy meeting on Sept. 17, with long-term bond yields dropping sharply and the Dow Jones Industrial Average soaring 900 points to a new record high.

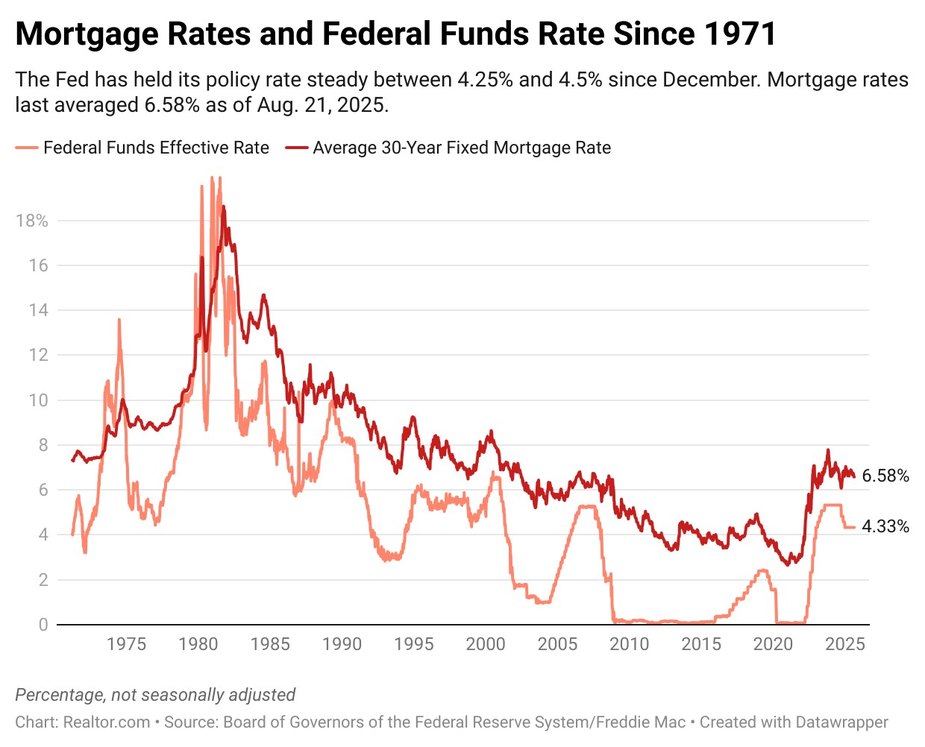

Fearful of lingering inflation, Powell and the other members of the Federal Open Market Committee have held the Fed’s benchmark rate steady at a range of 4.25% to 4.5% since December.

Mortgage rates have remained in the upper 6% range since then, adding to affordability challenges in the housing market and weighing heavily on home sales.

While the Fed doesn’t set mortgage rates directly, expectations about future Fed policy can influence them. That means mortgage rates often rise or drop well before the Fed changes its benchmark rate.

Mortgage rates matched a 10-month low this week at 6.58%, according to Freddie Mac, and following Powell’s comments, they should continue to dip further in the coming days. Still, homebuyers should not expect to see rates fall below 6% this year unless the economy takes a sharp downturn.

“In the short run, mortgage rates remaining at 10-month lows are already offering a boost to affordability and, potentially, to buyer sentiment,” says Realtor.com® senior economist Jake Krimmel. “That relief is welcome after several years of high borrowing costs eroded consumers’ purchasing power, leaving this summer especially frustrating for buyers, sellers, and builders as both existing- and new-home sales stayed sluggish.”

The heightened prospect of a September rate cut also boosted homebuilder stocks, with shares of Lennar, DR Horton, and Toll Brothers all rising more than 5% in morning trading on Friday.

Homebuilders have suffered under a double whammy from high rates, which raise their own financing costs for new projects as well as mortgage rates for customers.

Single-family home construction has suffered, with a total of 621,000 homes currently under construction in July, 3.7% lower than a year ago.

Beyond September, Powell offered little clarity about the Fed’s path on interest rates, saying that “monetary policy is not on a preset course.”

“FOMC members will make these decisions, based solely on their assessment of the data and its implications for the economic outlook and the balance of risks,” he said. “We will never deviate from that approach.”

Those comments were the closest Powell came to rebutting Trump’s demands for deep, immediate cuts to the Fed’s benchmark rate, which the president has pointed out would reduce refinancing costs for substantial federal debt that will roll over this fall.

Trump, who also promised much lower mortgage rates during his campaign, has for months demanded dramatic cuts to the Fed’s policy rate, at various points threatening to fire or sue Powell in his attempts to pressure the central bank to cut rates.

The president has used social media as his bully pulpit to press for lower rates, insulting Powell as feckless and foolish for holding rates steady.

“Could somebody please inform Jerome ‘Too Late’ Powell that he is hurting the Housing Industry, very badly? People can’t get a Mortgage because of him,” Trump wrote on his Truth Social site late Tuesday. “There is no Inflation, and every sign is pointing to a major Rate Cut. ‘Too Late’ is a disaster!”

On Wednesday, Trump-appointed housing regulator Bill Pulte took the campaign a step further, publicly accusing Fed Gov. Lisa Cook of lying on a mortgage application and calling for her ouster.

Pulte published a copy of a letter he wrote to Attorney General Pam Bondi recommending a criminal investigation into Cook on suspicion of falsifying bank documents and committing mortgage fraud in relation to a 2021 mortgage on a condo in Atlanta.

The letter alleges that she falsely claimed the condo would be her primary residence, and then months later listed it as available to rent.

“How can this woman be in charge of interest rates if she is allegedly lying to help her own interest rates?” Pulte wrote in a post on X.

Cook responded in a statement that she had “no intention of being bullied to step down” by a tweet, but that she planned to gather information about her financial history to answer any questions about the mortgage in question.

Trump, meanwhile, has threatened to fire Cook if she does not resign. Firing Cook for cause would allow Trump to replace her with an ally, and put him closer to controlling a majority on the FOMC, which has traditionally operated as a nonpartisan and independent body.

The criminal allegations against Cook open up a new front in the pressure campaign on Fed policymakers.

Appointed by President Joe Biden in 2022, Cook was one of the eight FOMC members who backed Powell in holding rates steady at the latest policy meeting last month.

Meanwhile, Fed Govs. Michelle Bowman and Christopher Waller dissented, voting for a quarter-point rate cut, marking the first time since 1993 that more than one FOMC member has diverged from the consensus.

On Wednesday afternoon, minutes from that FOMC meeting were released to the public, showing how opinions diverged on the panel when it came to weighing the dual risks of inflation and a recession in the labor market.

“Participants generally pointed to risks to both sides of the Committee’s dual mandate, emphasizing upside risk to inflation and downside risk to employment,” the minutes noted. While “a majority of participants judged the upside risk to inflation as the greater of these two risks,” a couple saw “downside risk to employment the more salient risk.”

Recent economic data showing a massive downward revision to recent employment numbers may change that equation, showing that the labor market is weaker than previously thought.

But inflation has also flashed troubling signs, with core CPI jumping back above 3% in July and wholesale inflation making the biggest monthly gain in three years.

Powell’s keynote address at the Fed’s annual conference in Jackson Hole marks his swan song at the symposium before his term expires in May.

In addition to offering guidance for September, the Fed chair also unveiled a new five-year policy framework for the Fed that could have implications that last long beyond his term.

Powell said the Fed is moving away from its 2020 strategy of flexible average inflation targeting and back toward a simpler flexible inflation-targeting approach, better suited to an economy where both inflation and employment risks matter.

“The new consensus statement restores a simpler flexible inflation-targeting framework and clarifies how the Fed balances its dual mandate when inflation and employment objectives diverge,” says Krimmel. “Put differently, the Fed is now more willing to lean against labor market weakness, even if inflation is still a touch high.”

Keith Griffith is a journalist at Realtor.com covering housing policy, real estate news, and trends in the residential market. Previously, his work has appeared in Business Insider, The Street, Chicago Sun-Times, New York Post, and Daily Mail, among other publications. He has a master’s degree in economic and business journalism from Columbia University.